[ad_1]

Whilst the March 2022 forecast update mirrored the affect of

Russia’s invasion of Ukraine, the April update addresses some

more troubles that have arisen, including a instead sluggish

recovery in semiconductor materials, the effect of additional COVID

lockdowns in China and the for a longer time-phrase impact of large uncooked

product rates that will place additional tension on new motor vehicle

affordability.

“At the moment the best chance to the outlook will come from the

menace of further more or prolonged lockdowns in mainland China and the

contagion into previously pressured global source chains,” reported Mark

Fulthorpe, Govt Director, World-wide Creation Forecasting,

S&P International Mobility.

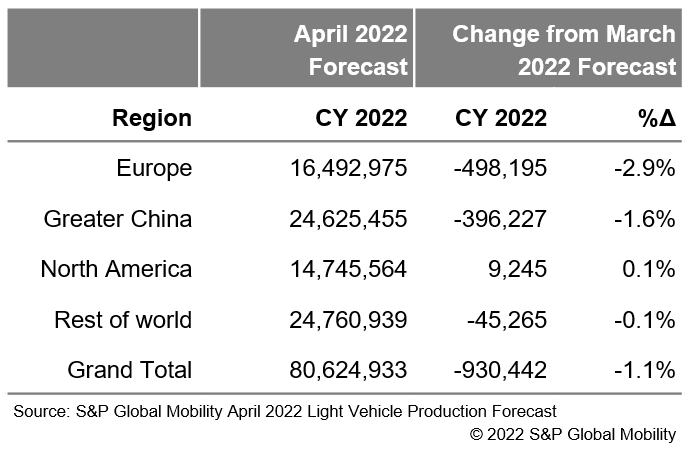

The April 2022 forecast update displays noteworthy reductions

for a number of marketplaces, with the most significant reductions targeted

on Europe and Bigger China.

The subsequent reflects the S&P World-wide Mobility April 2022

Mild Car or truck Manufacturing Forecast update:

The extra noteworthy regional adjustments with the hottest

forecast update are specific down below:

- Europe: The outlook for Europe light car

production was decreased by 498,000 units for 2022. With the April

update, we see European production remaining challenged as the

location proceeds to navigate the Russia/Ukraine impact as effectively as

ongoing provide chain problems. - Higher China: The outlook for Increased China

light car output was minimized by 396,000 units for 2022.

Closely hit by strict COVID containment measures, light-weight auto

output in March is approximated to have declined by 8% a

12 months-more than-12 months. In April, the Omicron variant has unfold to

Shanghai and pressured local federal government officers to employ

extensive lockdowns. As the affect of lockdowns expanded

from auto creation to pieces generation, ingredient shortages

are predicted to interrupt car production outdoors of Shanghai in

the in the vicinity of-expression, top to more car output effects in

adhering to months. - North The united states: In spite of the backdrop of the

Russia/Ukraine conflict and ongoing offer chain difficulties, the

outlook for North American gentle car production in 2022 remains

flat at 14.75 million units. Manufacturing in Q1-2022 arrived in a bit

higher than forecast with 3.55 million units manufactured. Nonetheless,

output in Q2- 2022 was revised down on continued source chain

struggles and worries surrounding supplemental logistics problems at

border crossings amongst the US and Mexico in Texas that could

exacerbate now strained ailments in the near-phrase.

This report was posted by S&P Worldwide Mobility and not by S&P World-wide Rankings, which is a separately managed division of S&P World wide.

[ad_2]

Supply link